From Policy to Practice

Financial Promotion Compliance

in UK Retail Offer Platforms

A review of the Winterflood Retail Access Platform (WRAP)

Key findings

- •Almost half of WRAP retail offers with available price data had negative 30-day returns. The worst-performing offers saw declines of up to 70%, and the issuers with the largest losses correlate with the compliance concerns identified elsewhere in this report.

- •Social media promotion during deal windows consistently lacked risk warnings. Directors, issuers, and brokers posted promotional content referencing active WRAP offers on X and LinkedIn without the disclosures required under FCA FG24/1. Zero LinkedIn posts examined contained a risk warning.

- •Issuers with going concern uncertainty raised retail capital via WRAP while disclosing material doubt about their ability to continue as a going concern, including explicit warnings that failure to raise funds would result in insolvency.

- •A cluster of bitcoin treasury companiesused WRAP to raise retail capital at extreme discounts with aggressive social media campaigns and no financial promotion consideration. These companies pivoted from their original business to bitcoin — retail investors may not have understood what they were subscribing to.

- •Investor presentations during live offers included direct solicitation language(“this is a good time, we’re cheap”) and unqualified revenue projections (“£20 million of revenue per month”), broadcast on video platforms outside standard compliance monitoring.

1. About this review

This review was commissioned by Retail Book Limited and undertaken independently by Copia, a financial communications firm with over 20 years’ experience in investor relations, capital markets communications, and regulatory reporting. Copia operates Ticker, a live company data platform providing real-time access to RNS announcements, director dealings, share price data, and issuer profiles across the London Stock Exchange and AQSE. Copia has long worked with ShareSoc, the UK Individual Shareholders Society, and is acutely aware of the importance of retail investor protection.

For this review, we analysed 211 RNS announcement bodies across 74 WRAP deals and 58 issuers, social media activity on X and LinkedIn from directors, issuers, and brokers during deal windows, 28 video transcripts from investor presentation platforms, and share price performance data for all WRAP issuers where market data was available. The underlying dataset covers the period from January 2025 to April 2026.

RetailBook has raised concerns about promotional practices in the WRAP ecosystem with the FCA through its quarterly regulatory dialogue. This report provides the evidence base supporting those concerns.

This is not a call to restrict retail access. It is an evidence-based assessment of how well the current framework serves the investors it is designed to protect.

2. Context

The Secondary Capital Raising Review, led by Mark Austin CBE in 2022, recommended that retail investors should participate in secondary fundraises by default — a welcome reform that this review supports in principle. The Public Offers and Admissions to Trading Regulations (POATR), which came into force in 2026, further simplify the framework for retail-inclusive IPOs and secondary fundraises.

The Investment Association’s Risk Warnings Review concluded that standardised risk warnings are widely misunderstood, often ignored by experienced investors, and can actively deter appropriate long-term investing. This finding is directly relevant to the evidence in this report: the question is not whether risk warnings should exist, but whether the financial promotions accompanying retail offers meet an adequate standard when retail participation is the default.

The government’s Industry Investment Campaign, launching on 23 April 2026, aims to encourage greater retail participation in UK capital markets. The quality of the promotional practices that accompany retail offers will directly affect whether that campaign builds lasting trust or exposes new investors to poor outcomes.

The Winterflood Retail Access Platform (WRAP) is operated by Winterflood Securities Limited (FRN 141455), a subsidiary of Winterflood Business Services. WRAP distributes retail offers alongside institutional placings, enabling existing shareholders and, in some cases, new investors to subscribe for shares in public companies via their stockbroker. In the period reviewed, WRAP facilitated 74 deals across 58 issuers.

Following the collapse of London Capital & Finance, the FCA introduced strengthened rules through PS23/13 and the section 21 financial promotion gateway, designed to ensure that authorised firms take meaningful responsibility for the promotions they approve or communicate. The evidence in this report tests whether that objective is being met in practice within the WRAP ecosystem.

3. Findings

3.1 Social media and financial promotions

We examined social media activity from directors, issuers, and brokers during WRAP deal windows across X and LinkedIn. The pattern is consistent: promotional content referencing active WRAP offers uniformly lacks the risk warnings and disclosures that the FCA’s rules require.

Zero LinkedIn posts examined contained a risk warning

FCA FG24/1 confirms that financial promotion rules are platform-agnostic. Posts directing investors to subscribe, referencing deal terms, or using promotional language about active offers appear to constitute financial promotions without appropriate risk warnings.

Serval Resources— LinkedIn company page

“LAST CHANCE! A great investment idea for the start of the new ISA year.” The post directed people to email WRAP@winterflood.com to participate, constituting a direct call to action with urgency language and no risk disclosure.

LinkedIn, 7 April 2026[https://www.linkedin.com/company/serval-resources/] · No risk warning · Names WRAP@winterflood.com

David Lenigas[https://x.com/DavidLenigas] (Vinanz / London BTC Company) — 138 tweets

Non-Executive Chairman of Vinanz, a bitcoin treasury company that raised over £3m across three WRAP offers. Lenigas posted 138 tweets during deal windows directing retail investors to WRAP, including five tweets in two hours on one occasion.

“Don’t be shy to call your broker / adviser to enquire and research the opportunity”

The share price fell 70.5% within 30 days of the second WRAP raise.

@DavidLenigas, 13 Jun 2025[https://x.com/DavidLenigas/status/1933401739220169200] · No risk warning

Freddie New[https://x.com/freddienew] (B HODL) — 97 tweets, weekly IR campaign

CEO of B HODL, a bitcoin treasury company that raised £15.3m via an Aquis IPO including a £2m WRAP retail offer. New posted weekly investor updates on personal X and LinkedIn naming $HODL ticker symbols, ATM programme commentary, and treasury operations — all with no risk warnings or s.21 approval.

“I encourage you all to continue using and holding your bitcoin as you see fit, ignoring their paltry and ineffective attempts… If they won’t listen, we route round them.”

The CEO of a company that raised retail capital through a regulated platform simultaneously encouraged investors to bypass FCA-imposed protections using VPNs.

@freddienew, 2 April 2026[https://x.com/freddienew/status/2039719970498543860] · On circumventing FCA geo-blocks

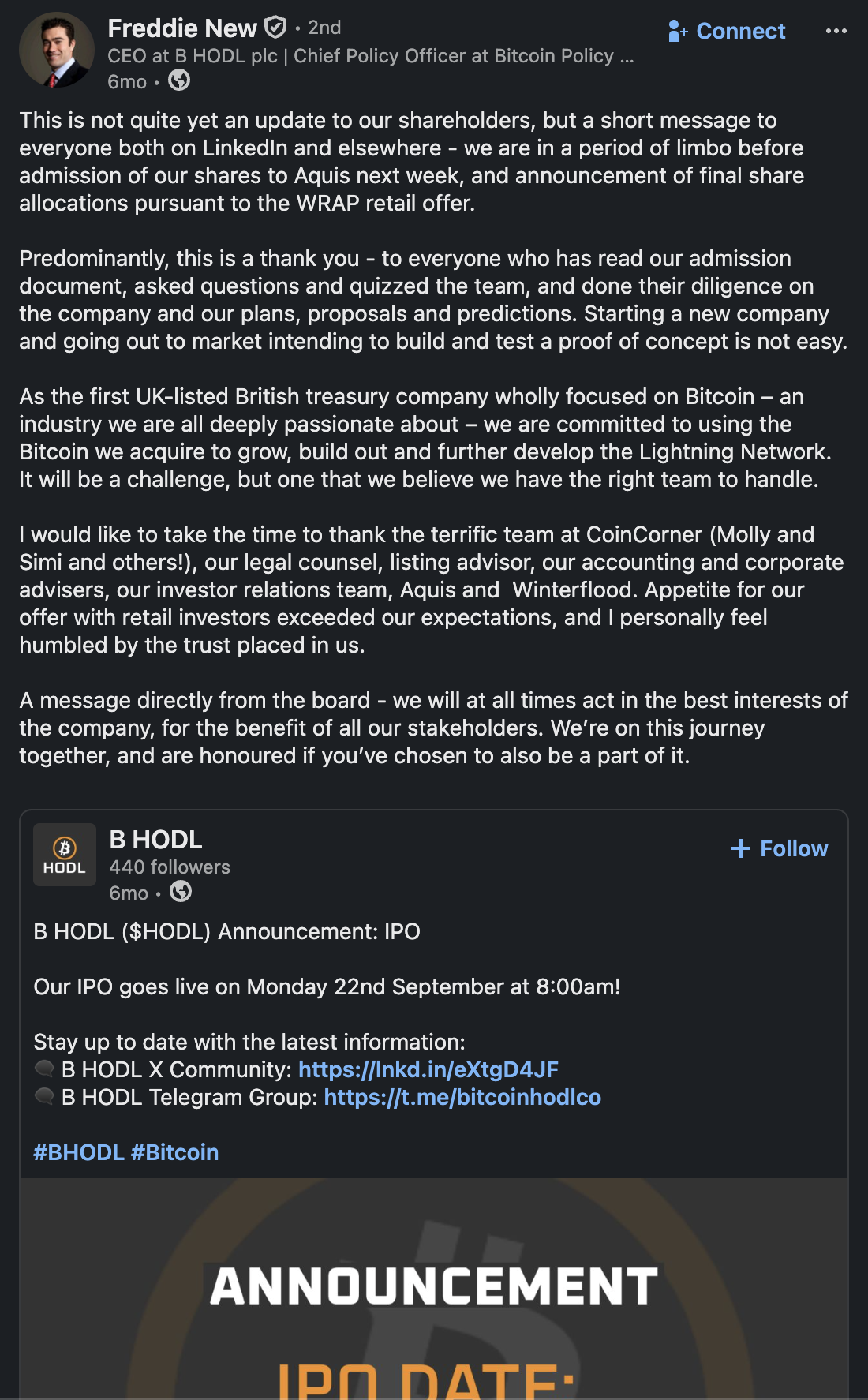

Freddie New[https://x.com/freddienew] (B HODL) — LinkedIn, pre-admission

During the pre-admission period, New posted on LinkedIn describing the WRAP retail offer and stating “appetite for our offer with retail investors exceeded our expectations.” The post included links to the B HODL X Community and Telegram group, and reposted the company’s IPO date announcement.

“A short message to everyone both on LinkedIn and elsewhere — we are in a period of limbo before admission of our shares to Aquis next week, and announcement of final share allocations pursuant to the WRAP retail offer.”

No risk warnings. The CEO used personal social media to promote an active retail offer to a public audience during the offer window.

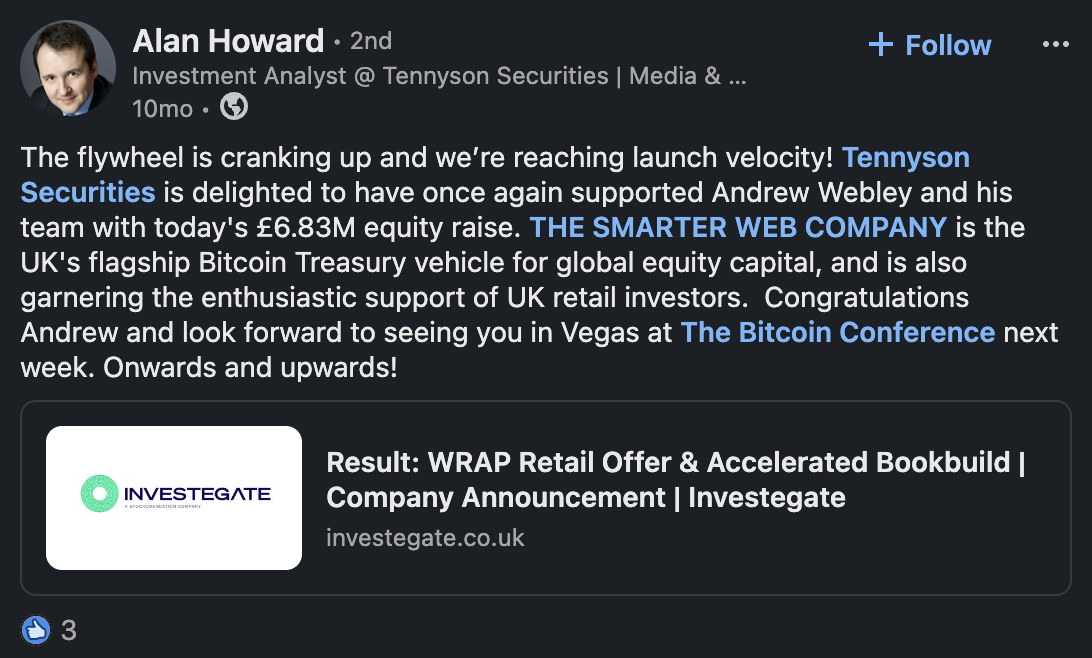

Alan Howard, Tennyson Securities (The Smarter Web Company) — LinkedIn

“The flywheel is cranking up and we’re reaching launch velocity!… the UK’s flagship Bitcoin Treasury vehicle for global equity capital… Onwards and upwards!”

The broker described the WRAP retail offer and accelerated bookbuild for The Smarter Web Company’s bitcoin treasury strategy with no risk warnings. SWC conducted four WRAP raises in four weeks, raising £6.3m from retail investors.

LinkedIn, 23 May 2025[https://www.linkedin.com/posts/alan-howard_result-wrap-retail-offer-accelerated-bookbuild-activity-7331730681594589184-ZnH-] · No risk warning

Sundae Bar— LinkedIn company page

“sundae_bar launches WRAP retail offer for Bitcoin treasury acquisition as part of our new Bitcoin Treasury Management Policy… We believe #digitalassets serve as an effective store of value and inflation hedge”

The issuer promoted its WRAP retail offer on LinkedIn with unqualified investment claims about digital assets as a “store of value and inflation hedge” — forward-looking claims presented without risk warnings or any acknowledgement of the FCA’s position on bitcoin as a high-risk asset.

LinkedIn · No risk warning · Investment claims

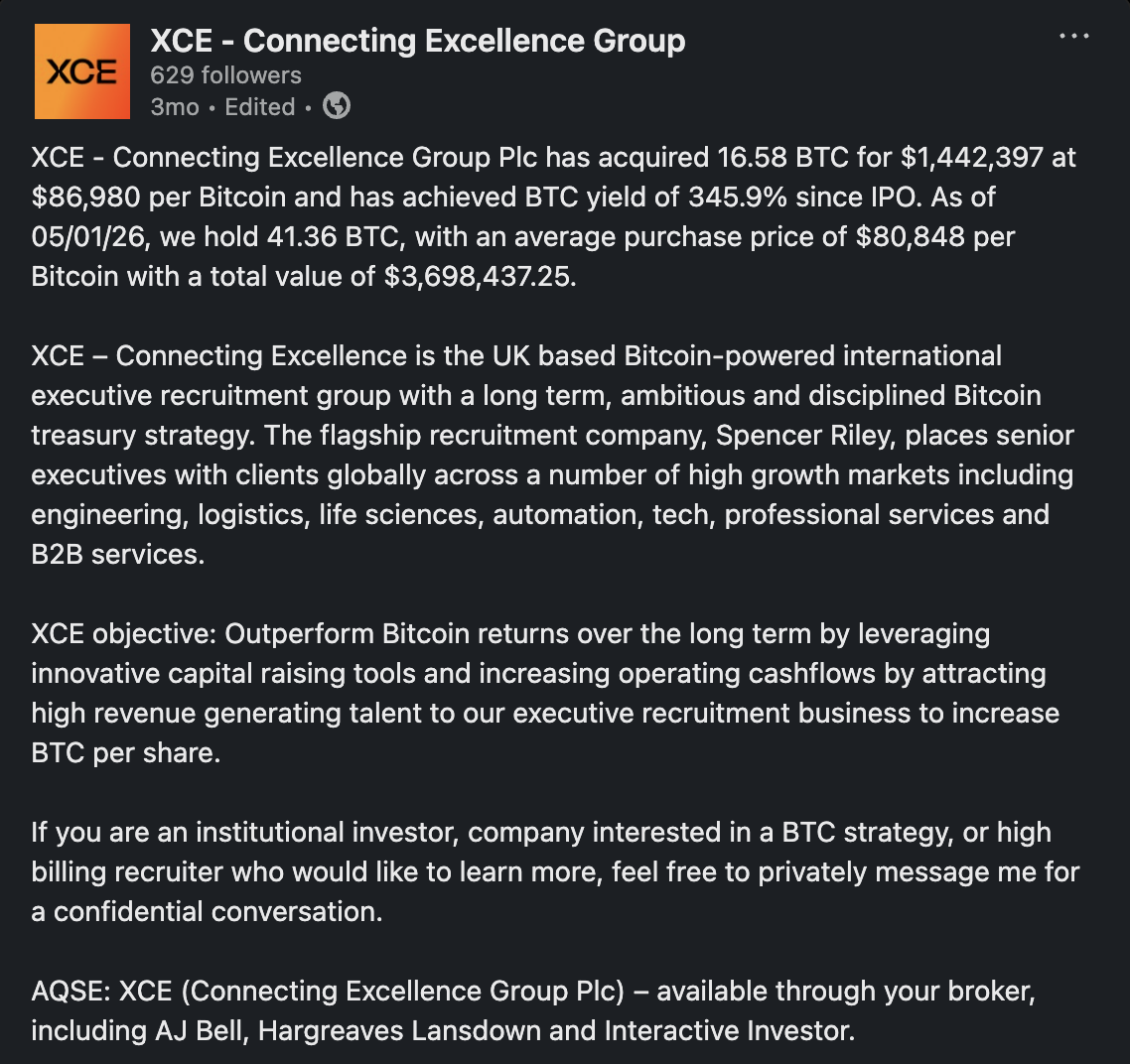

Connecting Excellence Group (XCE)— LinkedIn company page

“Outperform Bitcoin returns over the long term… available through your broker, including AJ Bell, Hargreaves Lansdown and Interactive Investor.”

The post makes an unqualified investment performance claim, invites institutional investors and recruiters to “privately message me for a confidential conversation”, and names three specific retail broker platforms — all with no risk warnings.

LinkedIn · No risk warning · Investment claim · Names broker platforms

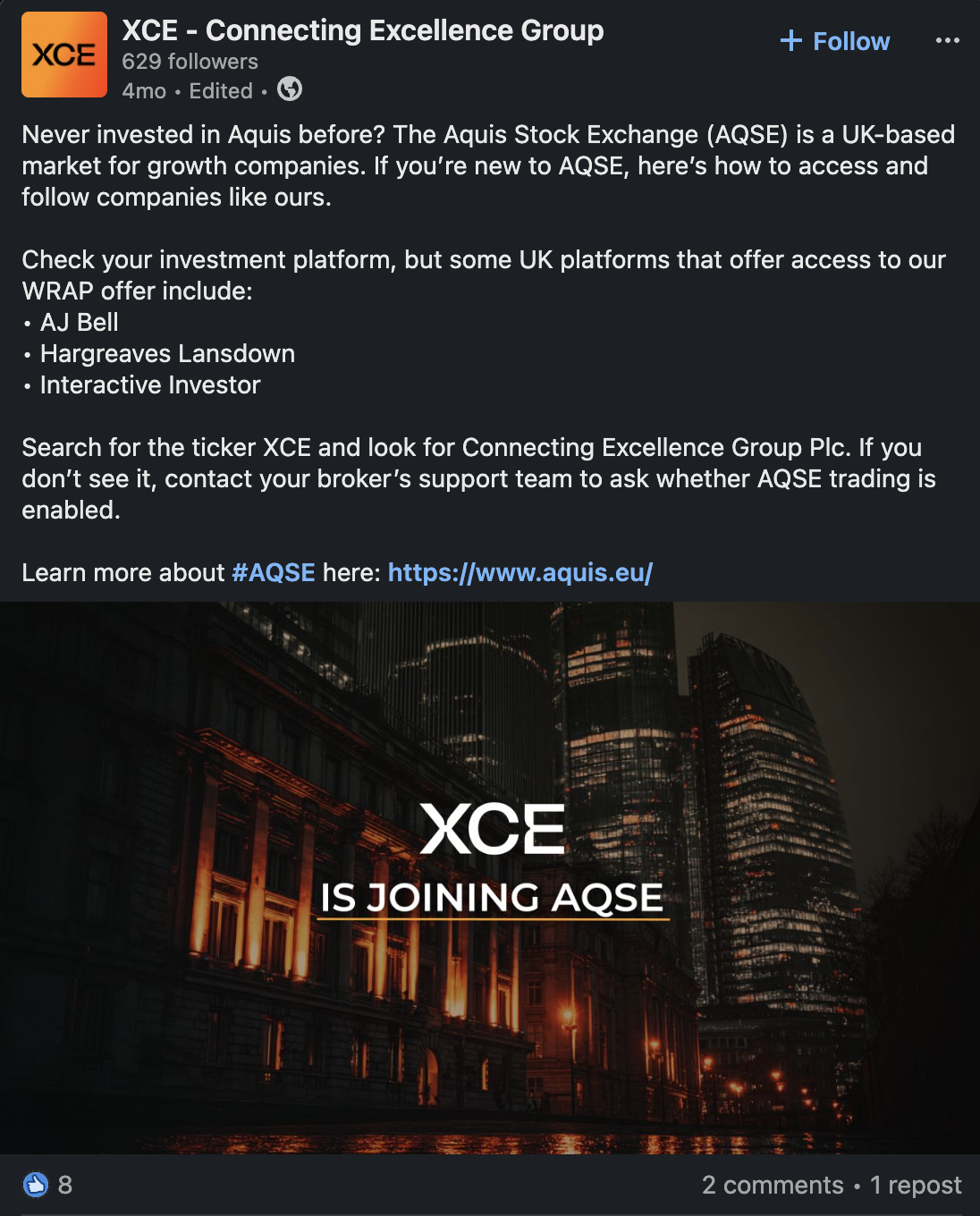

Connecting Excellence Group (XCE)— “Never invested in Aquis before?”

A post framed as educational guidance on how to buy AQSE-listed shares, naming AJ Bell, Hargreaves Lansdown, and Interactive Investor as platforms that “offer access to our WRAP offer”. Instructs readers to “search for the ticker XCE” and contact their broker to enable AQSE trading.

This is a bitcoin treasury company directing retail investors to specific platforms to purchase its shares, with no risk warnings or s.21 approval.

Winterflood Securities CEO & Head of Execution Services — B HODL, LinkedIn

Winterflood Securities CEO Bradley Dyer and Head of Execution Services Andrew Stancliffe both reposted B HODL’s LinkedIn announcement that the WRAP retail offer was “now open to UK retail investors”. The reposted content included a direct link to participate and a “WRAP OPEN” graphic with no risk warnings.

The CEO of the authorised firm operating WRAP personally amplified unregulated promotional content for a bitcoin treasury IPO, raising questions about the boundary between the platform’s regulatory responsibilities and the promotional ecosystem surrounding the offers it distributes.

3.2 Investor presentations during live retail offers

Several WRAP issuers held investor presentations on video platforms during active retail offer windows. These presentations ranged from moderately promotional to aggressively soliciting, and in most cases were conducted without the risk balancing or disclaimers that would be expected in a financial promotion.

CleanTech Lithium plc (CTL)

“If you, any of your audiences out there looking to buy, this is a good time. I think we’re cheap and it’s a good opportunity to come in.”— CleanTech Lithium CFO, Ticker TV interview, 20 February 2025[https://www.youtube.com/watch?v=0hdulB8ea1Q]

The video title itself referenced the retail offer and “strong newsflow”. The CFO explicitly invited viewers to buy shares during a live WRAP offer.

“I will outline what I would do if I was an existing shareholder”— Daniel, Fox Davies Capital, Investor Meet Company presentation, 10 February 2025[https://www.youtube.com/watch?v=roH35wYP3GQ]

In this separate presentation[https://www.youtube.com/watch?v=roH35wYP3GQ] ten days earlier, the Fox Davies Capital representative opened with a disclaimer that the session was “neither a solicitation nor an offer to participate”, then proceeded to outline deal terms, explain how private investors could participate via the broker option, and state what he would do as an existing shareholder.

MedPal AI plc (MPAL)

“That’s potentially 20 million of revenue we can run through that facility each month”— MedPal AI CEO, Vox Markets interview, 2 October 2025[https://www.youtube.com/watch?v=zT9ulZPm-V0]

“If you’re one of the only companies, if not the only company that is public… that you can invest in”— MedPal AI CEO, StockBox interview, 3 October 2025[https://www.youtube.com/watch?v=iFNTOvhfYmo]

Two media appearances in two days during an active WRAP offer window, both containing unqualified revenue projections with no risk warnings. The 30-day return following this offer was −17.6%.

Seascape Energy Asia plc (SEA) — s.21 multimedia approval

Winterflood extended section 21 approval to both a PDF presentation and a pre-recorded YouTube webinar[https://www.youtube.com/watch?v=rRDOA251LNE] published on the same day as the WRAP retail offer. The RNS states explicitly that the “presentation and pre-recorded webinar… has been approved for the purposes of Section 21 of the Financial Services and Markets Act 2000… by Winterflood Securities Limited”.

The webinar was a 49-minute geological presentation — largely technical in nature — but the CEO’s closing remarks included unqualified forward-looking projections with no risk balancing beyond the moderator’s standard introduction.

“We’ve got a portfolio here which could deliver north of 40,000 barrels a day of production to this company, who today sits at the market cap of 50 million quid and zero production. And that is a huge future.”— Nick Ingrassia, CEO, Seascape Energy Asia, Investor Meet Company webinar, 13 October 2025[https://www.youtube.com/watch?v=rRDOA251LNE]

Winterflood explicitly approved this content under s.21 FSMA — the question is whether the forward-looking projections in the CEO’s closing remarks met the standard expected of an approved financial promotion.

The regulatory gap: video platforms such as Vox Markets, StockBox, and Investor Meet Company operate editorially, but issuers use them for promotional purposes during live offers. This activity falls outside the section 21 framework unless the authorised firm explicitly extends its approval, as Winterflood did for Seascape Energy.

3.3 Going concern distress alongside retail offers

Several issuers raised retail capital via WRAP while their most recent financial statements disclosed material uncertainty about their ability to continue as a going concern. In each case, retail investors were being asked to subscribe to shares in companies whose own boards or auditors had flagged the possibility of insolvency.

Europa Oil & Gas (Holdings) plc (EOG)

“Should the resolution not be passed, the placing will not proceed, and the Company will not have sufficient funds to maintain its current interest in the EG-08 licence… nor to continue its other operations and there would be a material uncertainty over the Company’s ability to continue as a going concern.”— Europa Oil & Gas, WRAP Retail Offer RNS, 10 February 2026

The 30-day price change following the offer was +5.7%, though the explicit going concern language represents the most direct example of distress-driven retail solicitation in the dataset.

Sunda Energy plc (SNDA)

“Conditional subscriptions totalling £800,000… comprising (i) the conversion of £750,000 of the £1.5 million unsecured loan provided by Andy Butler (CEO of Sunda Energy)… and (ii) conditional subscriptions by three other directors… totalling £50,000.”— Sunda Energy, WRAP Retail Offer RNS, 8 April 2026

The CEO converted £750,000 of a personal unsecured loan into equity alongside a £750,000 WRAP retail offer and a 100:1 share consolidation. Board insiders took approximately 40% of the overall fundraising. The October 2025 WRAP offer saw a 30-day price decline of 20.3%.

Gelion plc (GELN)

Gelion disclosed in investor presentations that cash was sufficient only to January 2026, with a solvency assessment referenced. In an Investor Meet Company presentation[https://www.youtube.com/watch?v=8wFvYO3Wl8g] during the offer window, the CEO stated this was “simply the most exciting time for Gelion since I’ve been a CEO” and a non-executive director implied the shares were undervalued, stating the private valuation would be “significantly different”.

3.4 Bitcoin treasury pivots funded by retail capital

A cluster of companies used WRAP to raise retail capital in support of bitcoin treasury strategies. These companies had pivoted from their original business to bitcoin accumulation — retail investors may not have fully understood what they were subscribing to.

Vinanz Limited / London BTC Company (BTC) — David Lenigas[https://x.com/DavidLenigas]

Vinanz conducted three WRAP raises in three months (June–July 2025), raising over £4 million from retail investors for a pure bitcoin treasury strategy. CEO David Lenigas posted 138 tweets during this period, including five tweets in two hours on one occasion directing retail investors to the WRAP offer.

“Winterflood WRAP Retail Offer, to open up investment opportunity to all UK retailer investors”— David Lenigas, @DavidLenigas, 3 Jul 2025[https://x.com/DavidLenigas/status/1940637141387673644]

“Don’t be shy to call your broker”— David Lenigas, @DavidLenigas, 13 Jun 2025[https://x.com/DavidLenigas/status/1933401739220169200]

The share price fell 70.5% within 30 days of the second WRAP raise. The company subsequently renamed itself London BTC Company Limited.

The Smarter Web Company Plc (SWC)

The Smarter Web Company conducted four WRAP raises in four weeks (May–June 2025), raising £6.3 million from retail investors for a bitcoin treasury strategy. The early raises were majority-retail funded — 60% and 65% retail capital — before institutional money arrived in the later rounds. The issue price rose from 16p to 81p across the four raises.

| Date | Retail | Institutional | Retail % |

|---|---|---|---|

| 7 May 2025 | £1.35m | £0.90m | 60% |

| 14 May 2025 | £2.23m | £1.22m | 65% |

| 22 May 2025 | £2.31m | £4.52m | 34% |

| 4 Jun 2025 | £0.40m | £13.0m | 3% |

Retail investors provided the majority of capital in the first two raises, effectively bootstrapping the bitcoin treasury strategy before institutional capital followed at higher prices.

Sundae Bar plc (SBAR)

Separately AIM-listed Sundae Bar — also associated with the bitcoin treasury cluster — used WRAP to fund a Bitcoin Treasury Reserve Policy only weeks after IPO. A second WRAP raise four months later raised just £29,004 against a £100,000 target, with retail comprising only 3% of the total raise.

30-day returns: first raise +17.4%, second raise −13.8%.

B HODL / Freddie New[https://x.com/freddienew]

CEO Freddie New posted 97 tweets[https://x.com/freddienew] as part of a weekly investor relations campaign conducted through his personal social media account, with no risk warnings or s.21 approval.

Connecting Excellence Group (XCE)

An executive recruitment company that IPO’d on AQSE in December 2025 with a bitcoin treasury strategy built into its corporate model. The WRAP retail offer raised £500,000 (15% of the total £3.3m raise). XCE describes itself as “The Bitcoin-powered international executive recruitment company” and uses the same “dual-flywheel” language as The Smarter Web Company.

The company’s LinkedIn posts include a graphic directing people to buy shares “through your broker, including AJ Bell, Hargreaves Lansdown and Interactive Investor” — naming specific broker platforms with no risk warnings. BTC holdings are promoted with a “437% year-to-date BTC yield” graphic, again with no risk warnings.

The share price has fallen approximately 36% from its first day of trading. Michael Crosbie, also associated with B HODL, appears connected to XCE.

These companies pivoted from their original business tobitcoin or listed with bitcoin treasury strategies from day one. The RNS announcements describe the use of proceeds as “bitcoin purchases to strengthen our overall treasury position” and adoption of a “Bitcoin Treasury Reserve Policy”. Retail investors subscribing through their stockbroker may not have appreciated the nature of the underlying investment.

A coordinated promotional network

These bitcoin treasury companies do not operate in isolation. A LinkedIn review of Falconedge (AQSE: EDGE) board advisor Stefania Barbaglio (15,600 followers) identified a single post cross-promoting seven bitcoin treasury companies simultaneously: Falconedge, B HODL, The Smarter Web Company, Connecting Excellence Group (XCE), Stack BTC PLC, BTC Treasury Group, and Capital B — all tagged as LinkedIn company pages in one post. Scott Ellam (XCE CEO) is named personally. No risk warnings.

Falconedge’s CEO Roy Kashi promotes specific yield figures (“4.07% balance sheet growth”) with only informal crypto jargon (“NFA and DYOR”) as a disclaimer — not FCA-compliant. CIO Benny Menashe claims “20x the performance of peers” with specific BTC holding data and no risk warnings.

The cross-promotional activity, shared advisory relationships, consistent “flywheel” terminology, and shared personnel — Michael Crosbie holds roles at both B HODL and XCE — suggests a coordinated ecosystem rather than independent adoption of bitcoin treasury strategies. Retail capital raised via WRAP is funding entry into this ecosystem.

3.5 Consumer outcomes — price performance

Of the WRAP retail offers where 30-day price data was available, almost half had negative returns. The worst outcomes correlate with the issuers flagged elsewhere in this report for compliance concerns — the seven offers with the largest declines all involve issuers identified in this review for other reasons.

| Issuer | Offer date | Retail % | 30-day return | Context |

|---|---|---|---|---|

| Vinanz / London BTC | 2 Jul 2025 | 70% | −70.5% | Bitcoin treasury, 138 CEO tweets |

| Sunda Energy | 15 Oct 2025 | 66% | −20.3% | CEO loan conversion, 100:1 consolidation |

| MedPal AI | 1 Oct 2025 | 27% | −17.6% | Video solicitation during offer window |

| Vinanz / London BTC | 12 Jun 2025 | 100% | −17.5% | First WRAP raise, no institutional |

| Physiomics | 13 Feb 2025 | 14% | −16.2% | Two WRAP raises in 7 days |

| Gelion | 16 Oct 2025 | 5% | −14.3% | Going concern context |

| Sundae Bar | 28 Oct 2025 | 3% | −13.8% | Bitcoin treasury pivot, second raise |

Under PRIN 2A (Consumer Duty), firms distributing financial products to retail customers must act to deliver good outcomes. The concentration of negative post-offer returns, particularly among issuers with compounding risk factors, raises questions about the adequacy of due diligence and risk disclosure in the WRAP distribution process.

4. Observations and areas for consideration

The section 21 approval landscape is inconsistent

Of 211 RNS bodies reviewed, only 20 carry explicit Winterflood Securities s.21 approval language. Fifty-one rely on the FPO Article 43 exemption (communications to existing shareholders). The remaining announcements contain varying degrees of compliance language. This inconsistency makes it difficult for investors — and for regulators — to determine which entity has taken responsibility for the promotional content.

Social media activity around fundraises uniformly lacks risk warnings

The tweets and LinkedIn posts analysed during deal windows present a consistent pattern: directors, issuers, and brokers post promotional content referencing active offers without the disclosures required by FCA rules. This activity is platform-agnostic under FG24/1 and appears to constitute unregulated financial promotion.

The gap between formal RNS approval and informal multimedia promotion

In most cases, the only content subject to s.21 approval (or Article 43 exemption) is the RNS announcement. The accompanying social media, LinkedIn posts, investor presentations, and video interviews operate in a parallel channel with lower or no compliance standards. This creates an uneven information environment where the regulated communication is the least engaging content, and the most persuasive content is unregulated.

Post-LCF reforms and the s.21 gateway

The regulatory reforms introduced through PS23/13 were designed to ensure that authorised firms take meaningful responsibility for the promotions they approve. The evidence in this report raises questions about whether that objective is being met in practice. The Seascape Energy example — where Winterflood explicitly approved multimedia content — demonstrates that extension of s.21 liability to video is possible, but it remains the exception rather than the norm.

Consumer Duty obligations extend beyond the RNS

Firms involved in distributing retail offers have Consumer Duty obligations under PRIN 2A that extend to the entire customer journey — not only the RNS announcement but also the marketing, information environment, and post-offer outcomes. Where almost half of retail offers produce negative 30-day returns and social media solicitation is conducted without risk warnings, the question of whether good consumer outcomes are being delivered is a reasonable one for the regulator to consider.